In late February, as Russia began its large-scale invasion of Ukraine, the energy world flew into high alert, bracing for major disruptions to energy markets that remain highly dependent on Russian oil and gas. The fallback was swift, prompting an unprecedented volatility that has reverberated across the world.

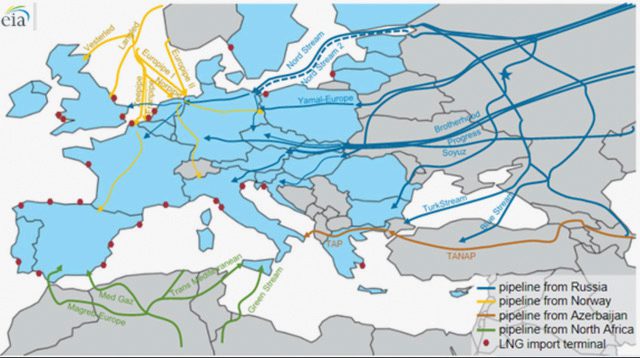

1. While pipeline imports of natural gas into Europe come from Russia, Norway, North Africa, and Azerbaijan, imports originating in Russia—the largest supplier in the region—grew from about 11 billion cubic feet per day (Bcf/d) in 2010 to more than 13 Bcf/d in 2020, which was a low-consumption year owing to the pandemic. Despite construction of new pipelines, imports from Norway averaged around 9 Bcf/d between 2010 and 2020. Growing volumes of flexible liquefied natural gas (LNG) imports, which made up about 26% of all natural gas imports into Europe in 2020, primarily from the U.S. contributed to the notable increases in LNG imports to Europe from 2019 to 2021. Source: U.S. Energy Information Administration

While Russia—the world’s second-largest producer of natural gas and third-largest producer of oil—threatened to restrict energy exports, as of March 11, the energy giant continued to send natural gas through its gas pipeline infrastructure to feed 30% of European gas demand (Figure 1). But in Europe, which has long been stalked by the risk of a flow interruption and supply squeeze, countries have moved urgently to look for new gas supply sources as part of international penalties aiming to isolate Moscow. Following Germany’s decisive certification halt of the Nord Stream 2 Baltic Sea gas pipeline project—an $11 billion project completed in September that was slated to double the flow of Russian gas to Germany—the U.S. has so far announced a complete ban on Russian oil, gas, and coal imports, and the European Union (EU) issued an urgent roadmap to make Europe independent of Russian fossil fuels by 2030.

The recent shock is compounding tension that had been building in gas markets over the past year. Since September 2021, Europe has fielded an acute post-pandemic energy crisis stemming from a “perfect storm” of factors, including a sharp rebound of Asian demand (particularly in China) for liquefied natural gas (LNG), various supply constraints (including a fire at a major Siberian processing plant), and climate-conscious cuts to upstream investments.

By October, as global climate talks at the United Nations Climate Change Conference (COP26) renewed scrutiny of the natural gas industry’s role in reducing anthropogenic methane emissions, discussions were underlaid by pleas for pragmatism, with reliability and affordability suddenly agleam in sustainability strategies. And as winter cold spells triggered a spike in demand in Europe, Asia, and North America, prices have trundled upward.

In January, high gas prices in Europe, which relies on natural gas for 20% of its total generation, sent average wholesale prices soaring to more than four times their 2015–2020 average. In the U.S., Henry Hub natural gas prices more than doubled compared to their 2020 average of $4.60/MMBtu in the second half of 2021—their highest level since 2008. And in Japan and South Korea, while oil-indexed LNG prices rose less strongly than in other regions, surging coal prices and renewable supply chains’ sluggishness are bolstering natural gas power’s competitive position.

The Volatility of Gas Supply

At least in the short term, most analysts agree that global power prices in 2022 will continue to reflect the ongoing tightness and volatility of the global gas market. According to IHS Markit, the dynamics that led to the 2021 energy supply crunch “are not expected to moderate in 2022.” The firm, which became part of intelligence firm S&P Global days before its annual international energy-focused CERAweek conference in Houston (now known as CERAWeek by S&P Global), said that though slowing economic and electricity demand growth in China, the U.S, and other large economies could “reduce pressure on the demand-side,” it may not be enough to ease ongoing market tightness.

Given the blowback against Russia, a prominent winner may be the LNG industry because its key contribution is flexibility, Michael Smith, chairman, CEO, and founder of Freeport LNG, suggested at CERAweek in March. While traditionally a seasonal commodity, the last two years have been exceptionally volatile, swinging from oversupply in early 2020 to surging demand and high prices at the end of 2021, he noted. “Every LNG terminal in the world has been running flat out, and we found out that we do not have any excess LNG in the system,” Smith said. A recent wave of supply agreements span China and other parts of Asia, but the sector’s ongoing mitigation of Europe’s energy crisis has highlighted new value for the fuel. “The idea behind U.S. LNG is there’s no destination restrictions—it’s completely flexible,” said Smith.

However, the LNG sector faces material risks, including a possible supply deficit by 2024. New capacity, however, is hampered by mixed investment signals, and investment signals hinge on commercial, political, regulatory, and public appetite for new gas projects. According to Smith, action now is imperative, given “these plans take years and years to build.”

Marco Alvera, CEO of Italian infrastructure firm Snam, also highlighted a dire need for infrastructure, though he proposed the sector’s flexibility could be heightened with more storage and accompanying joint pricing mechanisms. “With only €2 billion of extra storage investments, we could store about 312 TWh or 30 Bcm of energy in summer and use that in winter to essentially make Europe almost import-free during the winter,” he said.

Modern gas pipelines will also factor heavily into future gas power plays. But according to Cynthia Hansen, executive vice president and president of Gas Transmission and Midstream at pipeline firm Enbridge, government carbon priorities will determine how that plays out. “We have to provide more energy security, both for Europe and for North America,” she said. “We still have places in North America where you have that disconnect in the U.S. Northeast because we haven’t been able to build out our pipeline infrastructure.”

For U.S. natural gas suppliers, a glaring new issue is the Federal Energy Regulatory Commission’s (FERC’s) February-issued sweeping new guidance for new interstate natural gas facilities, Hansen noted. The energy regulator has moved, for the first time, to consider whether a proposed project fulfills environmental interests—including of proposed mitigation of greenhouse gas (GHG) emissions—and interests of landowners and surrounding communities. The policy has “introduced some increasing ambiguity into the process where pipeline infrastructure is being asked to do assessment of upstream and downstream impacts, and that is not adding to the clarity of the process,” said Hansen.

An Evolving Landscape for Gas Power

Complexities swirling around gas suppliers are evidently bearing down on the gas power industry, putting unsustainable pressure on end-users. Reacting to these developments, some governments have stepped in with stop-gap measures to bail out energy firms and customers veering on the brink of collapse. At least five of the biggest European economies —Germany, the U.K., France, Italy, and Spain—have so far rolled out grants and time-limited tax cuts to help consumers heat and power their homes.

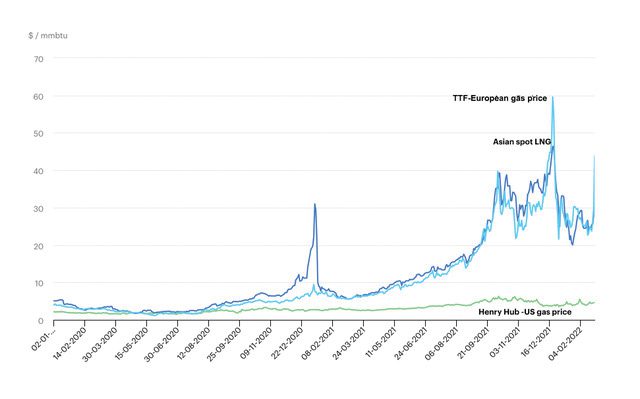

2. European natural gas prices have in the past year risen to all-time highs and remain extremely volatile. Courtesy: International Energy Agency (IEA), Natural gas prices in Europe, Asia and the United States, Jan 2020–February 2022, IEA, Paris

“European power prices are a direct reflection of what we’re seeing happening in the commodity markets,” noted Catherine Robinson, S&P Global executive director, in March. “Gas prices in Europe are trading at around €240 to €150/MWh—that’s $50/MMBtu—seven to 10 times normal levels.” With coal prices that hover around $400 per ton, high fuel costs (Figure 2) are feeding directly into current power prices in the EU that are now in excess of €300/MWh.

“I think it’s really important to say, however, that these do not reflect scarcity pricing from point of view of power, these €300/MWh prices are a direct reflection of the entries in the dispatch cost for thermal generation in the EU,” said Robinson. “So, really, what we’re seeing in Europe today from a power perspective is not as it is normally from a commodity perspective, but from a power perspective. It’s an affordability crisis.”

The impact can be felt even in Asia, where shares of gas generation are relatively small, and the fuel supply mix is less dependent on spot prices, said S&P Global’s Jenny Yang. What’s significant, however, is in the short term—and particularly in China where gas power makes up 3% of total generation—these impacts have persuaded generators to fall back on domestic coal resources, she said. “I think a lot of other markets in Southeast Asia share very similar challenges as China,” Yang said. Other countries like Japan and South Korea are meanwhile concertedly exploring nuclear again. Japan is slated to restart several reactors this year to offset LNG generation, and South Korea recently elected Yoon Suk-yeol, a new president who supports policies that favor nuclear.

In the U.S., prices “will look similar to what they did last year on both gas and power,” suggested Douglas Giuffre, S&P Global senior director. “Certainly sub-$5, possibly sub-$4. So, not changing certain fundamentals a whole lot in the external markets, and certainly not in the near-term.” Prices will continue to play a key role in determining gas generator profitability, particularly in competitive markets, which are being increasingly saturated with renewables, he said.

Investment trends, however, could lean more heavily on clean energy portfolios (CEPs)—combinations of wind, solar, energy efficiency, demand response, and battery energy storage—which appear to be gaining momentum as an alternative to building new gas plants, according to RMI, an independent nonprofit that works with entities to identify and scale climate-related “energy system interventions.” CEPs represented over 90% of new capacity entering interconnection queues in 2020, while a “combination of economics and advocacy has led to the cancellation prior to construction of more than 50% of proposed new gas plants in the past two years,” RMI noted. Economic and policy headwinds associated with gas power include resiliency concerns and health burdens, it said.

The Glimmer in Technology

Despite these challenges, the world’s biggest gas technology equipment manufacturers remain optimistic that gas generation will thrive—at least over the near term. “Our view is very consistent with many of the third parties, such as IEA, IHS Markit, [BloombergNEF], and others, that gas is going to experience growth through at least 2030. And that’s growth in gas generation globally,” Brian Gutknecht, marketing leader at GE Power, told POWER in February. Beyond 2030, multiple scenarios may begin to diverge, with some scenarios anticipating stronger growth for gas power equipped with carbon capture through 2040, he noted.

Growth this decade will be founded on gas generation’s “critical” net-zero role. Gas power’s GHG emissions can be a third of coal’s, according to some estimates that factor in efficiency, but gas also offers “the flexibility and dispatchability needed to balance intermittent renewables and variable renewables, and providing some of the system inertia that’s required for system resilience. On top of that, you’ve got demand growth projected to be about a 50% increase by 2040,” Gutknecht noted. “A lot of that demand growth is going to happen in developing economies in Asia, where they already currently account for about two-thirds of global [carbon dioxide] emissions.”

A key misconception frequently shrouding the energy conversation, though sometimes underscored in gas power forecasts, is technology’s potential to decarbonize gas, Gutknecht noted. “Some of those scenarios see rapid growth, not just in natural gas but in abated gas—so gas with carbon capture, gas [and] hydrogen,” he said. Gas “is part of the solution,” he said. “It really is. These third parties are saying it actually is critical to achieving our climate objectives and growth in gas is critical to doing it at the speed and scale that’s required.”

Erik Zindel, vice president of Generation Sales of Hydrogen at Siemens Energy, agreed. The build-up and capacity availability of gas power plants is “required to cover the residual load demand resulting from the fluctuating renewables,” he noted. But significant demand growth could also come from increased sector coupling and the electrification of other energy-intensive sectors, such as mobility, industry, or buildings.

“With ‘H2 -ready’ plants, which are already prepared for a later upgrade to 100%-hydrogen operation, these new gas power plants will be ready to provide full decarbonized residual power in electricity grids dominated by fluctuating renewable energy. So, natural gas serves as bridge-fuel whilst the gas power plant itself is a future-proof technology and a key enabler to fully decarbonize the power sector,” he said.

“Basically, that’s not all wishful thinking, as the technologies for realizing this vision are available in principle,” Zindel added. “Even gas turbines capable of firing 100% hydrogen will be ready long before the market demands it. And finally, from a cost perspective, it should be noted that fully decarbonizing the power sector is manageable and no longer a roadblock.”