June 2021 saw the first electricity flows across Britain’s latest interconnector, the 1.4GW North Sea Link (NSL) with Norway. The interconnector will commence full operation on 1 October, supplying GB with relatively cheap, low carbon electricity imports.

Recent analysis from Cornwall Insight looks into this new interconnection and assesses what impacts the NSL will have on the GB market. NSL will have an annual transmission capacity of 12.3TWh, and we can expect to see net imports as high as 10TWh per year to the GB. Based upon total electricity demand from 2019-20 (~290TWh), this would mean that the NSL could provide an equivalent of 4.2% of the GB’s annual electricity demand.

The Norwegian power market is currently split into five Bidding Zones, each with its own wholesale power price. The NSL will connect to Kvilldal in Bidding Zone 2 and will more broadly be connecting into one of the lowest priced power markets in Europe.

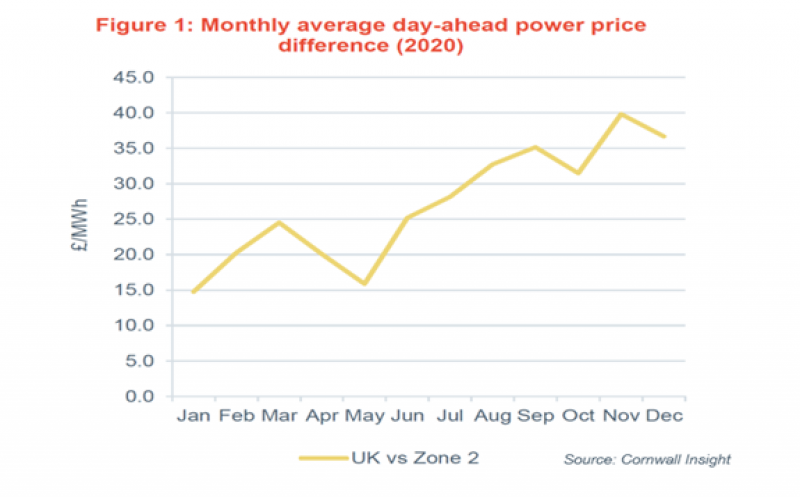

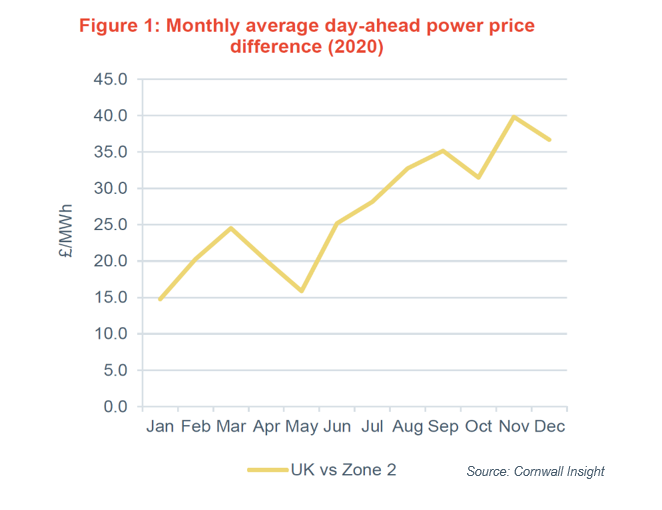

This is due to the higher power prices with the GB market regularly outturning at a premium against Norway, as highlighted below. We can see the extent of this price differential in Figure 1, with the monthly average power price in the GB between £14.7/MWh and £39.9/MWh higher than its Norwegian counterpart throughout last year.

Joe Camish, Analyst at Cornwall Insight, said:

“From an operational perspective, the rollout of the new interconnector will mean GB will be able to benefit from Norway’s cheaper energy to help balance its growing capacity of intermittent renewables. Norway could also expect to import from GB during high renewable, low demand periods to preserve its hydro capacity for peak demand periods.

“Back in December 2014, Ofgem produced an initial project assessment of the interconnector. The evaluation suggested that the NSL would benefit consumers by “reducing the wholesale price of electricity, improving the operation of the GB transmission system, and increasing the security of supply”. Throughout the 25-year cap and floor regime, Ofgem’s Base Case scenario forecast benefits to GB consumers of ~£3.5bn. The report also noted that in the same scenario, the average annual domestic consumer bill would decline by around £2.0 due to the NSL.

“However, this likely will not be the case for consumers in Norway, with studies anticipating increased Norwegian demand due to the higher exports associated with the NSL, which will raise Norwegian power prices by between 20-25kr/MWh, equivalent to £1.7-2.1/MWh.

“Lastly, its deployment is also expected to aid in meeting the GB’s net zero targets. With Ofgem noting back in 2014 that the NSL could assist the reductions in long-term GB carbon emissions due to more efficient renewables dispatch – i.e., making better use of GB wind and Norwegian hydro resources. National Grid, a partner in the project with Statnett, agree with this view.

“The development of the NSL is just one of many similar projects over the coming years, as GB bolsters its interconnector capacity. As a result, the GB market can expect to see an additional 1.4GW of new interconnection next year.”