Now, we’re left watching and waiting to see to what extent (if at all) the current stimulus talks in congress, as well as negotiations on upcoming bills, will consider the renewable power sector’s recent push for modification and extension of tax incentives amidst the flood of cheap oil. This initiative is backed by some Democrats. This is an important consideration, as Axios points out, because “solar and wind industry groups are starting to provide early projections of the economic fallout as the frozen economy hits development and coronavirus forces workers home.”

According to Axios’ reporting, the Solar Energy Industries Association sent a memo along with a letter that officially proposed an economic stimulus strategy for the renewables sector which “cites analysts' estimates of ‘losses between 16% and 30% of volume this year and some sectors could see as much as 50% reduction,’” potentially resulting in “jobs losses in the 38,000–120,000 range, a huge chunk of the sectors' roughly 250,000 workforce.” The wind power sector, not to be left out, reported (via the American Wind Energy Association) that “roughly 25 gigawatts worth of planned project [...] representing $35 billion worth of investment” and “35,000 jobs” could soon be on the chopping block.

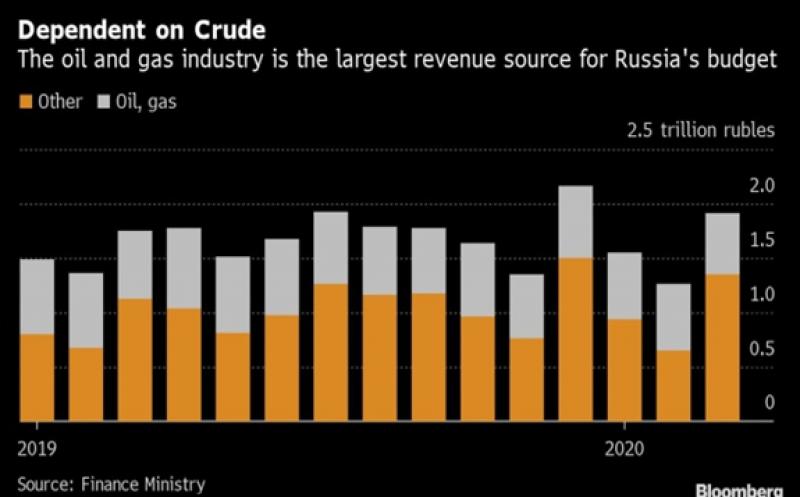

And that’s just a small portion of the havoc being wreaked by the oil crash. Even though the crash itself probably will not last long, the implications will be far-reaching. This certainly isn’t the first big oil crash, “but there will be at least one important and lasting difference this time around — and it has major market and geopolitical implications,” says the Financial Times. “The oil price crash is a foretaste of where the whole energy sector was going anyway — and that is down.”

Few could make the argument that the future of the energy industry lies in oil--or in any fossil fuel, for that matter. With each passing year, policymakers and industry leaders push forward clean energy campaigns and research, and in the last year, even Saudi Aramco had to admit that peak oil is likely just around the corner.

“It may not look that way at first,” warns the Financial Times. Saudi Arabia will soon ease its price war and reinstate lower production caps, Riyadh and Moscow will make amends, the world will recover from COVID-19, and the global economy will slowly recover. “Yet this inevitable bounceback should not distract from two fundamental factors that were already remaking oil and gas markets. First, the shale revolution has fundamentally eroded industry profitability. Second, the renewables’ revolution will continue to depress growth in demand.”

The death of fossil fuels is not imminent, but it is inevitable. So maybe it’s not such a bad idea to give a little boost to the renewable energy sector after all.