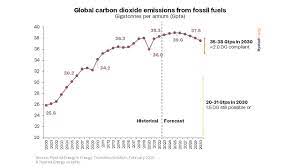

The inflection point for fossil fuel carbon dioxide (CO2) emissions is nigh, with emissions on track to peak by 2025, according to Rystad Energy research and analysis. On the current global pathway of announced policies, projects, industry trends and expected technological advancements, global CO2 emissions are poised to hit about 39 Gt/yr in 2025 before settling into a steady annual decline as industries clean up their carbon footprint.

Emissions hit a record high in 2022 as countries scrambled to secure reliable, affordable fuel for power generation on the back of Russia’s invasion of Ukraine. As a result, many turned to more carbon-intensive fuels as a short-term solution to their energy security crises, reviving mothballed coal plants and prioritising gas over cleaner alternatives. While these fuels will still have a role to play in the global economy for decades to come, the broader push towards a cleaner future is showing no signs of slowing down.

As a sign of things to come, direct CO2 emissions – CO2 originating from fossil fuel combustion at the plants worldwide – from power and heat generation will peak this year. The decline will be minimal initially before gathering momentum in the coming years, becoming a significant factor behind the decrease in total CO2 emissions from all sectors by 2025.

“Peak fossil fuel CO2 emissions within the next two years is an outstanding global achievement, exceptional when considering the current supply chain roadblocks and the high focus on energy security. If the industry can maintain this momentum, global warming of less than 2.0°C is within reach,” said Artem Abramov, head of clean tech research at Rystad Energy.

Fossil CO2 emissions reached an all-time high of about 38.3 Gt/yr in 2022, raising eyebrows and questions about the world’s ability to deliver on ambitious climate goals to limit warming to between 1.5 – 2.0°C. However, Rystad Energy's comprehensive emissions modelling points to an imminent emissions inflection point. The data shows a peak of 39 Gt/yr in 2025, but that timeline could move up to as early as next year if the short-term macroeconomic outlook accelerates the energy transition.

Power and heating to drive emissions reductions globally

2022 proved a challenging one for global climate goals. On the one hand, a record amount of new utility-scale solar and wind capacity was added – about 300 GW globally – triggering a sizeable increase in renewable-generated electricity, a trend that is likely to increase again this year. However, these new installations were weaker than forecast, thanks to low-carbon supply-chain disruptions and inflationary pressure. Moreover, Russia’s invasion of Ukraine fundamentally disrupted energy flows, resulting in widespread natural gas shortages, particularly in Europe, facilitating the increase in coal use for power generation. As a result, direct fossil CO2 emissions from the power and heat sectors hit record highs of around 14.4 Gt/yr.

Global industrial emissions (process and direct use of fossil fuels for energy generation purposes at industrial facilities) in 2022 stayed flat at ~9.95 Gt/yr as post-COVID-19 recovery in China was offset by a visible decline in Chinese industrial carbon intensity.

Transport emissions increased by 0.2 Gt/yr to reach 7.8 Gt/yr in 2022 – falling short of pre-COVID-19 peaks of 8.2 Gt/yr due to the continued weakness of the aviation sector, triggered by the pandemic and accelerating penetration of electric vehicles (EVs). EV adoption is approaching the levels needed to offset the annual global growth of the size of the active car fleet.

Despite these setbacks, the power and heating sector is expected to drive the upcoming fossil CO2 decline from mid-decade onwards. In 2023, the addition of renewable generation capacity is projected to outstrip the uptick in electricity demand. From 2025, annual renewable generation additions will start materially affecting total fossil fuel output. This trend will also accompany continuous coal-to-gas switching (the persistent trend established several decades ago net of occasional short-term disruptions). Transportation and industrial emissions will peak later this decade but are also expected to join the decarbonisation trend in the second half of the 2020s. At the same time, the first generation of large-scale commercial carbon capture initiatives will also start playing non-negligible roles, driven initially by projects in Europe and North America.

While Europe, the US and China make progress, India's emissions grow

The decarbonisation picture differs across regions, and key contributors of emissions are expected to play diverging roles in the coming years. For instance, Europe, the US and China are on track to reduce fossil CO2 emissions by 24%, 18% and 10%, respectively, by 2030. Europe and the US are on a path to structurally decarbonise their economies, leaning into newly implemented clean technology and low-carbon policies from 2025 onwards.

The Chinese transport sector is electrifying at a rapid speed, domestic renewable installations are strong, as is its low-carbon supply chain, and it is positioned for an acceleration in industrial decarbonisation for energy-intensive sectors in the next 5 – 10 years. As a result, Rystad Energy expects Chinese fossil CO2 emissions to plateau this year at about 12.5 Gt/yr before declining from 2026 through 2028.

At the other end of the spectrum, India is expected to continue its momentum of expanding CO2 emissions as its economy expands and the population grows. It is expected that Indian CO2 emissions will increase by 36% between 2022 – 2030, surpassing Europe in 2025 and the US in the early 2030s. Rystad Energy anticipates growing emissions to slow in the 2030s as non-coal power generation steps up to meet incremental electricity demand growth.

Elsewhere, industrial emissions are expected to increase by about 20% by 2030, driven predominantly by other Asian countries (excluding China), which are set to account for half of the increase in total fossil fuel emissions growth.