The U.S. shale industry is burning through cash so fast that even the state of Texas is looking at government rationed production targets. Texas Railroad Commissioner Ryan Sitton laid out his idea in an article for Bloomberg Opinion, proposing the commission institute a 10 percent production cut. It would mark the first time since the 1970s that the Railroad Commission regulated production.

Sitton twisted himself into knots in an attempt to characterize OPEC abandoning production cuts as “anti-market” while describing his proposal to require cuts as a return to free market principles. Orwellian as it may seem, some Texas shale drillers welcomed government intervention, including Parsley Energy and Pioneer Natural Resources.

Although production curtailments would boost oil prices, it could also destroy whatever shred of interest remains in the sector for investors. It remains to be seen if such an idea moves forward.

The fact that the shale industry finds itself in such a massive bind, facing an existential crisis and pleading with the state to impose regulation, is a perfect capstone to a decade of unprofitable drilling. A new report from the Institute for Energy Economics and Financial Analysis (IEEFA) offers an indictment of the industry’s financial performance.

A cross-section of 34 shale companies identified by IEEFA finds that they spent a combined $189 billion more than they earned over the past decade. That includes $2.1 billion in negative cash flow last year.

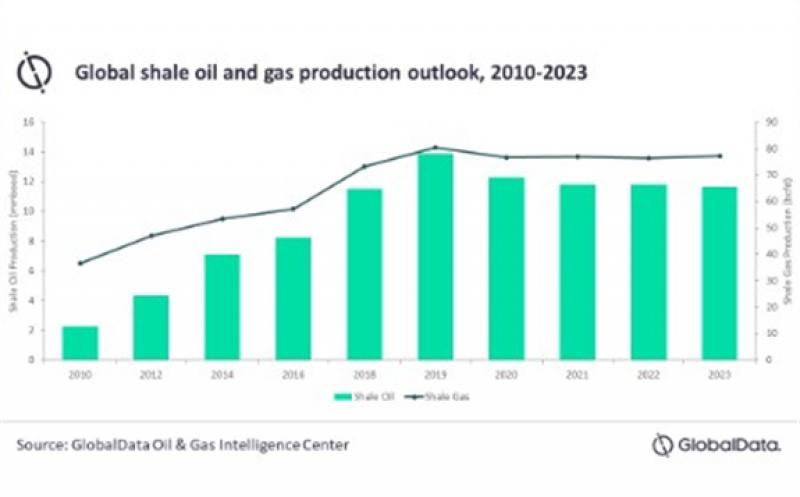

Over the past ten years, the shale industry has dramatically ramped up oil production, allowing the U.S. to become the world’s largest oil producer. “Yet in financial terms, this production boom has been an unrelenting financial bust,” IEEFA analysts wrote.

Notably, the 34 companies included in the analysis – which included large names such as Hess, Marathon, Pioneer Natural Resources, among others – posted negative cash flow in every single year over the past decade, IEEFA found.

While it might be understandable that drillers burned through cash during the 2014-2016 downturn, only six of the 34 companies surveyed by the institute reported positive cumulative cash flow between 2017 and 2019. That is a rather grim statistic for an industry that has hyped various mantras – low breakevens, technological innovation, big data and digitalization, downspacing and most recently, capital discipline – to justify why the next round of drilling might be different.

The energy sector was “far and away the worst performer of the S&P 500 over the past decade,” IEEFA notes, “placing dead-last among all sectors for stock price returns in both 2018 and 2019.”

That was all before the global pandemic and the collapse of the OPEC+ deal. With WTI in the mid-$20s, the shale industry is in a much more profound crisis. Prices may even go lower in the weeks ahead.

Sector-wide spending cuts and mass layoffs are in the works. Bankruptcies are set to multiply.

Mandatory production cuts from Texas regulators, which still seems unlikely, would do very little to erase the worldwide glut. The “supply cuts would however remain much too small to offset the current 8 mb/d hit on demand from the coronavirus…and wouldn’t prevent an unprecedented inventory build over the next months which could still saturate local logistical capacity and push prices to cash-costs,” Goldman Sachs wrote in a note.

The blistering growth rate of U.S. shale was already running on fumes at the start of the year, before the coronavirus spread around the world. Drillers were struggling at $50 WTI. With prices so far below that level at this point, the wheels are coming off of the shale complex.

“When and if global oil markets stabilize, investors should remain deeply skeptical of a shale-sector turnaround, given the industry’s financially feeble performance over the past decade,” IEEFA analysts concluded in their report. “Cautious investors would be wise to view shale-focused companies as high-risk enterprises characterized by disappointing performance, weak financial fundamentals, and an essentially speculative business model.”