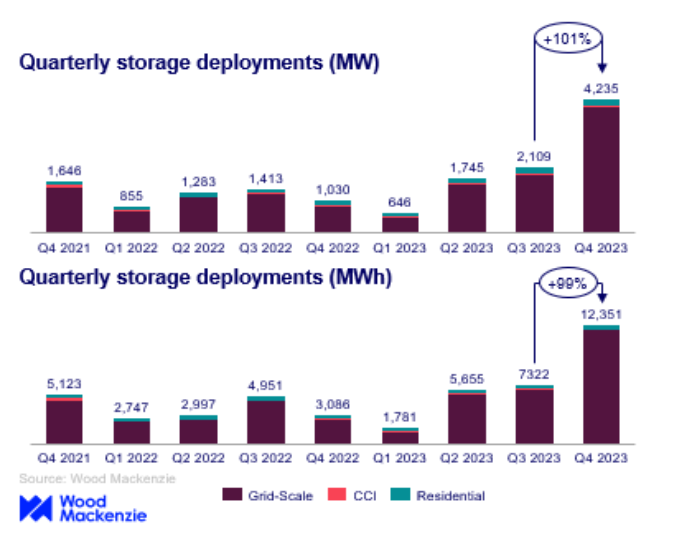

The US energy storage market broke previous records for deployment across all segments in the final quarter of 2023, with 4,236 MW/12,351 MWh installed over the period. That’s a 100% increase from Q3, according to a new report.

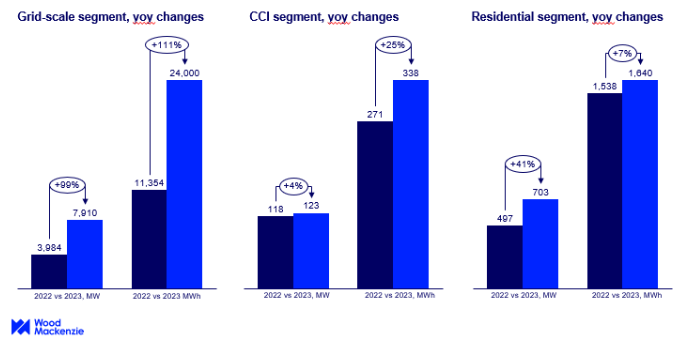

For the first time, the grid-scale segment exceeded 3 GW deployed in one quarter and nearly surpassed 4 GW alone, according to Wood Mackenzie and the American Clean Power Association’s (ACP) latest U.S. Energy Storage Monitor publication. 3,983 MW of new capacity additions represent a 358% increase compared to the same period in 2022.

“The energy storage industry continues its incredible growth trajectory, with a record quarter helping drive home a banner year for the technology,” said John Hensley, ACP’s Vice President of Markets and Policy Analysis. “These additions bring with them critical benefits to our power grid. Energy storage has unique capabilities to address grid resilience, with the ability to serve as generation, load, and transmission. These benefits to the grid have been evident, especially in recent years, as storage has provided reliability and stability during critical moments like historic heat waves. With a robust pipeline, the future for energy storage deployment is strong.”

For the US residential segment, deployments reached 218.5 MW, which slightly exceeded the previous quarterly installation record of 210.9 MW set in Q3 2023. Market gains in California were offset by a contraction in Puerto Rico, likely related to incentives.

“Q4 2023 was extremely strong for the US energy storage market, helped by easing supply chain challenges and system price declines,” Vanessa Witte, senior analyst with Wood Mackenzie’s energy storage team, said. “The quarter was commanded by deployments in the grid-scale segment, which recorded the highest quarter-on-quarter growth of any segment, ending the year with a 113% increase over Q3 2023. California continued to lead installations in both MW and MWh terms, closely followed by Arizona and Texas.”

The Community, Commercial, and Industrial (CCI) segment remained stagnant QoQ with 33.9 MW installed in Q4, where installed capacity was split relatively evenly between California, Massachusetts, and New York.

According to the report, total deployments in 2023 across all segments reached 8,735 MW and 25,978 MWh, representing an 89% increase over 2022.

Distributed storage exceeded 2 GWh in 2023, another first for the market. This was assisted by a busier-than-average first quarter for the CCI segment, and over 200 MW of installations in Q3 and Q4 each in the residential segment.

Over the next five years, the report says, the residential market will continue to boom, with more than 9 GW due to be installed. While the cumulative volume installed for the CCI segment is forecasted to be less than that, at 4 GW, the growth rate is over double, at 246%.

Earlier this year, the U.S. Energy Information Administration (EIA) said U.S. battery storage capacity could increase 89% by the end of 2024 if all of the planned energy storage systems reach commercial operation on schedule. Developers plan to expand U.S. battery capacity to more than 30 GW by the end of 2024. Planned and currently operational U.S. utility-scale battery capacity totaled around 16 GW at the end of 2023.

Battery storage in the U.S. has been growing since 2021. This is especially true in California and Texas, two states undergoing rapid renewable energy growth. California has the most installed battery storage capacity of any state with 7.3 GW and Texas has 3.2 GW. All other states combined have a total of around 3.5 GW installed capacity.