Opec's headquarters in Vienna. AP

The Opec+ alliance of 23 oil-producing countries has agreed to roll over its existing oil output cuts as the fuel demand outlook in China — the world’s second-largest economy and top crude importer — improves.

"The [Joint Ministerial Monitoring Committee] reaffirmed their commitment to the [declaration of co-operation] which extends to the end of 2023," said the group, which slashed its collective output by 2 million barrels per day in October last year.

The committee reviewed crude oil production data for the months of November and December and urged all participating countries to achieve "full conformity".

The next meeting of the JMMC is scheduled for April 3.

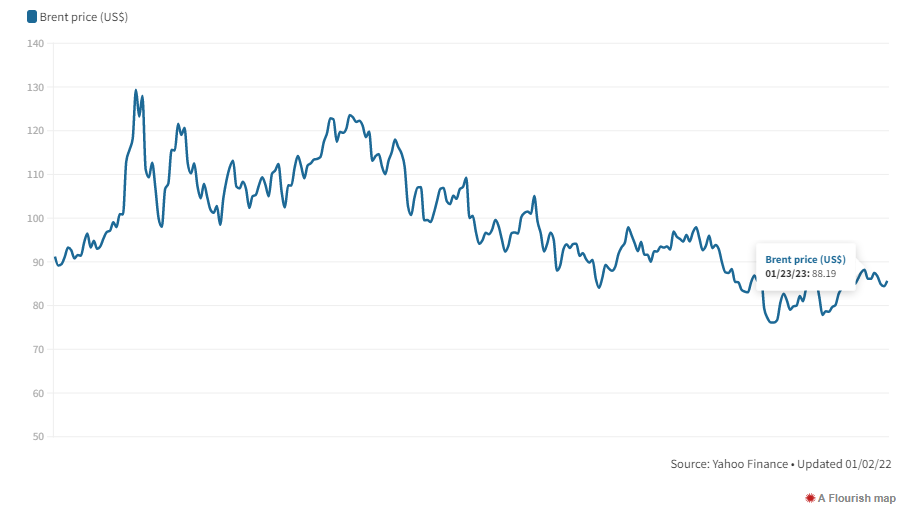

The announcement comes as oil prices have rallied by nearly 13 per cent since falling to a low of $76 last month, after China lifted Covid-19 restrictions and hopes grew that easing inflation would slow the rate of interest rate increases by central banks.

Brent, the benchmark for two thirds of the world’s oil, was down 3 per cent at $82.90 a barrel at 11.26 pm UAE time.

The International Monetary Fund on Tuesday marginally raised its global economic growth forecast for 2023, but said that more work needed to be done for a full recovery to take place.

The fund, which raised its economic growth estimate for this year to 2.9 per cent from a previous forecast of 2.7 per cent, said a depreciating US dollar, coupled with global monetary policy tightening, was starting to cool demand and inflation.

Meanwhile, global oil demand is set to reach record levels this year, supported by fuel demand recovery in top manufacturing hub China.

The International Energy Agency (IEA) has said the Asian country will account for nearly half of its 2023 oil demand growth forecast of 1.9 million bpd.

Research firm Energy Intelligence expects demand to grow to 101.2 million bpd this year, surpassing a previous record of 100.6 million bpd in 2019.

Although China represents 10 per cent to 15 per cent of global oil and gas demand, the country's recovery has not been entirely priced in by global commodity markets, according to Japanese bank MUFG.

The existing commodity prices do not “tally up” with China’s economic growth and “rapidly normalising” mobility in the country, said Ehsan Khoman, head of research — commodities, ESG and emerging markets at MUFG, in a report.

Energy markets are set to tighten further as an EU embargo on Russian crude products comes into effect on February 5.

The Group of Seven advanced economies is also considering a price cap on refined products from Russia, similar to the one the alliance imposed on Russia’s crude exports at the end of last year.

“Once the EU embargo on Russian seaborne fuel exports kicks in, we are likely to see prices for gasoline and especially diesel remain supported by tightening supply,” said Ole Hansen, head of commodity strategy at Saxo Bank, this week.

“Russia may, however, struggle to offload its diesel to other buyers, with key customers in Asia being more interested in feeding their refineries with heavily discounted Russian crude, which can then be turned into fuel products selling at the prevailing global market price,” said Mr Hansen.

Russian oil exports declined by 200,000 bpd last month after an EU crude embargo and the G7 price cap on the country’s crude shipments came into effect on December 5, according to the IEA.

The latest Opec+ meeting, the group’s third over the last four months, underlines its growing role in maintaining oil market stability as oil and gas producers in Europe and North America face supply constraints and rising investor pressure.

The supergroup would take a decision “that serves balancing the market”, Suhail Al Mazrouei, the UAE's Minister of Energy and Infrastructure, told reporters on the sidelines of an event in Abu Dhabi this month.

“With China reopening, hopefully, we will see a pick-up in the [crude] demand.”

Oil prices have been volatile since the start of Russia’s military offensive in Ukraine last February. After surging to a 14-year high of nearly $140 a barrel last March, Brent is currently trading in the $80 to $85 range.

“The biggest dangers to the oil price complex are actually coming from the potential demand destruction because of the Ukraine and Russia war and also under-investment,” Karen Kostanian, oil and gas analyst at Bank of America (BofA) Global Research, said at a media round-table last week.

Opec+ may have held its output steady at the last meeting fearing the demand destruction that would come with a recession, Mr Kostanian said.

Meanwhile, oil and gas exploration activity picked up pace last year after the pandemic had stalled or delayed several projects.

New oil and gas discoveries in 2022 could create at least $33 billion in value at Brent prices of $60 a barrel, according to Energy consultancy Wood Mackenzie.

While exploration well numbers were less than half the levels seen in pre-pandemic years, the total volume of 20 billion barrels of oil equivalent matched the average annual volumes from 2013 to 2019, Wood Mackenzie said.

“The highest value came from world-class discoveries in a new deepwater play in Namibia, as well as resource additions in Algeria and several new deepwater discoveries in Guyana and Brazil,” said Julie Wilson, director of global exploration research at Wood Mackenzie.

“The average discovery last year was over 150 million barrels of oil equivalent, more than double the average of the previous decade.”