A surprise rise in US crude stocks is weighing on futures

A trader at the New York Stock Exchange. Brent, which hit a 14-year high of $140 a barrel in March, has since lost most of its gains. Reuters

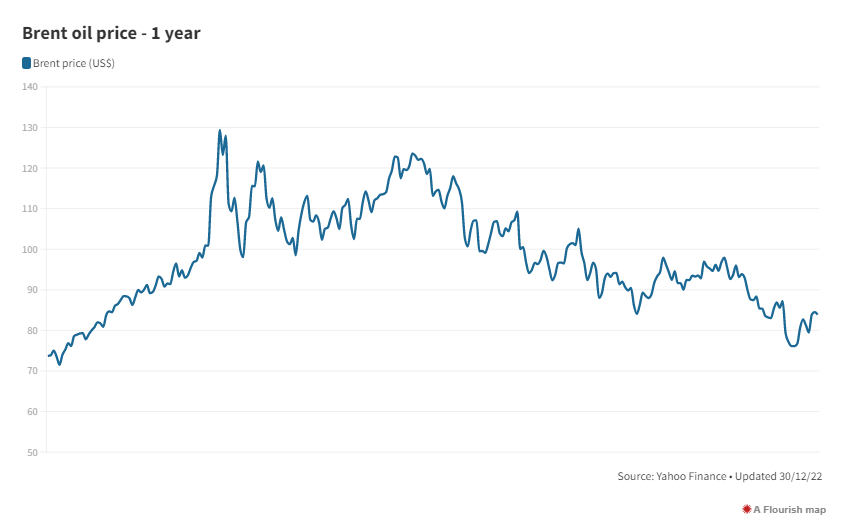

Oil prices ended the week higher on Friday, rallying on the last trading of the year, despite an unexpected rise in US crude stocks, recession fears and demand concerns owing to a resurgence of Covid-19 infections in the world's top crude importer China.

Brent, the benchmark for two thirds of the world’s oil, settled 2.94 per cent higher at $85.91 a barrel at the close of trading on Friday, while West Texas Intermediate, the gauge that tracks US crude, gained 2.37 per cent to $80.26 a barrel.

Despite the price volatility this year, which was exacerbated by the Ukraine war that disrupted global supplies, this was the second annual gain for the oil market.

Brent gained about 10 per cent this year, after jumping 50 per cent in 2021, while WTI ended up about 7 per cent in 2022, following a 55 per cent surge last year.

Brent soared to a 14-year high of close to $140 a barrel in March after Russia’s invasion of Ukraine, but sluggish economic growth in China and the strong possibility of a recession in several economies weighed on the market.

“Going into 2023, the risks are arguably tilted to the upside, although that has been the narrative for much of the year," said Craig Erlam, a senior market analyst at Oanda.

"While producers have finally caught up with post-pandemic demand, other risks remain next year, notably Russian output amid the new price cap and its threats to cut output and not supply any countries abiding by it. That isn't a problem now but if prices do start rising, that could accelerate the move quickly,” said Mr Erlam.

A surprise increase in US crude stocks weighed on prices at the start of trading on Friday.

US commercial oil inventories increased by about 700,000 barrels in the week ending on December 23, data from the US Energy Information Administration (EIA) showed.

Meanwhile, analysts were expecting crude stockpiles to fall by 700,000 barrels to 1.5 million barrels.

The indicator, which shows the level of oil and product stored, gives an overview of US petroleum demand. If the increase in crude stocks is more than expected, it implies weaker demand and is bearish for crude prices.

On Thursday, TC Energy said it completed a controlled restart of its Keystone crude pipeline to Cushing, Oklahoma, returning the vital oil link to service after a three-week shutdown.

"The Keystone Pipeline System is now operational to all delivery points. As always, we continue to monitor the system 24/7 as we deliver the energy customers and North Americans rely on," the Canadian pipeline operator said in a statement.

The pipeline, which can transport 622,000 barrels per day of oil, was closed after more than 14,000 barrels of crude oil spilled into a creek in Kansas.

Analysts and investment banks expect prices to rebound to about $100 next year as China reopens its economy and sanctions on Russian crude cause supply disruptions.

Swiss Lender UBS said earlier that oil demand growth would also be driven by India, Indonesia, South Korea and Malaysia.

"We had all kinds of speculation that it would rally to the $180-200 per barrel area … [but] recession fears took a toll on bullish bets," Ipek Ozkardeskaya, senior analyst at Swissquote Bank, said.

Earlier this week, Russian President Vladimir Putin signed a decree that banned the supply of oil and related products from February 1 for five months to nations that abide by a price cap on its exports.

On December 5, the EU, Australia and the Group of Seven advanced economies agreed to place a price cap of $60 on global purchases of seaborne Russian crude.

EU sanctions on Russian crude, including a ban on refined petroleum products that comes into effect on February 5, are expected to lead to a “further reallocation” of trade, according to the International Energy Agency.

Russia’s oil production could drop by 1.4 million barrels per day in 2023 as a result of the sanctions, the Paris-based agency estimated.

Meanwhile, the Opec+ group of oil-producing countries has shown its willingness to act quickly to protect high crude prices.

The group, which slashed its collective output by 2 million bpd, said this month that it would stick to its oil production targets.

But it is ready to address “market developments” and support the “balance of the oil market and its stability if necessary”.