The roadmap released by the Department of Energy (DOE) on Sept. 7 outlines four pathways that could dramatically transform how the five sectors, which account for 50% of the energy-related CO2 emissions in the industrial sector, produce and consume their energy. The pathways include energy efficiency, including use of smart manufacturing and advanced data analytics, and industrial electrification, which comprises leveraging low-carbon grid power, onsite renewable generation, and heat pumps. The roadmap also urges manufacturers to adopt low-carbon fuels, energy sources, and feedstocks, like renewable hydrogen, biofuels, and bio-feedstocks. The final pathway urges deploying carbon capture, utilization, and storage (CCUS), including the use of emerging technologies to reuse captured carbon.

The “Industrial Decarbonization Roadmap” also notably includes a targeted research, development, and demonstration (RD&D) agenda that will leverage a newly announced $104 million funding opportunity.

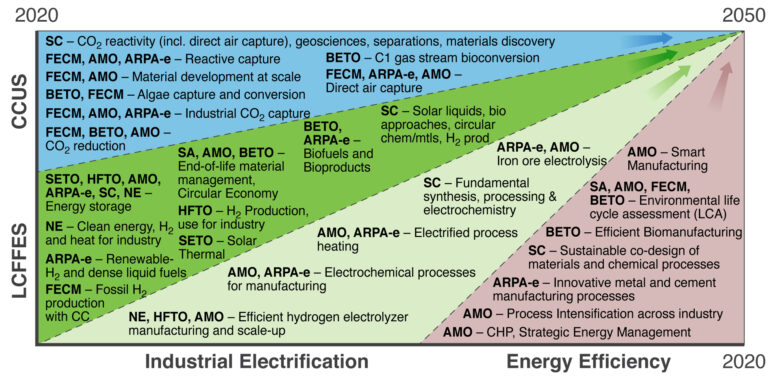

Landscape of DOE office activities across four decarbonization pillars to achieve net-zero emissions by 2050. Notes: LCFFES = Low carbon fuels, feedstocks, and energy sources. CCUS = Carbon capture, utilization, and storage. DOE Offices: AMO = Advanced Manufacturing Office; ARPA-E = Advanced Research Projects Agency–Energy; BETO = Bioenergy Technologies Office; FECM = Office of Fossil Energy and Carbon Management; HFTO = Hydrogen and Fuel Cell Technologies Office; NE = Office of Nuclear Energy; SA = Office of Energy Efficiency and Renewable Energy– Strategy Analysis; SC = Office of Science; SETO = Solar Energy Technologies Office. Source: DOE

A Closer Look at the Pathways

The roadmap spearheads a “cross-cutting” approach that leverages technologies, processes, and practices. The DOE’s chosen pathways—specific actions the U.S. can pursue—are based on four “pillars,” which represent “foundational elements” of the overall industrial decarbonization strategy.

The DOE said it chose the pillars “amongst a range of options due to their ability to provide step-change reductions, applicability across all industrial subsectors, and the capability to deliver near-term and future reductions as the [greenhouse gas (GHG)] emissions intensity of the electrical grid decreases, technologies develop (e.g., clean hydrogen), and hard-to-abate sources are addressed (by CCUS for example).”

Energy Efficiency. Using energy more efficiently in the industrial sector may be a key cost-effective option, given the sector’s generation and use of heat, including for process heating, boilers, and combined heat and power (CHP) systems. In U.S. manufacturing, steam accounts for 30% of process heat energy use, the DOE noted on Wednesday. However, the proportion of energy used for process heating varies by industry across broad ranges. Lower temperature ranges (below 150C) offer “the most significant energy reduction opportunities” for current and emerging technologies, the agency said. The agency also pointed to efficiency measures related to electrical energy consumption. Motor applications including pumps, fans, compressed air, materials handling, and others account for 91% of manufacturing electrical energy consumption, it said.

Energy efficiency efforts in the sector could come from investments in technology developments, for example, for energy-efficient process heating (even if it relies on fossil fuel combustion), until the grid can sustainably support electrification. Digitalization, including smart manufacturing and advanced data analytics, could also help unlock energy efficiency, the agency suggested.

The DOE also prominently highlighted the potential of CHP technology, particularly if switched over to emerging low-carbon fuels in the future, to tamp down energy losses. “Industrial CHP systems, through both topping and bottoming cycles, can provide needed energy services for some subsectors with overall energy efficiencies of 65%–85% compared to separate production of heat and power, which collectively averages 45%–55% system efficiency,” it says. “In particular, CHP is prevalent in chemicals, pulp and paper, refining, primary metals, and food industries, but can also be found in crop production, nonmetallic minerals, and other uses.”

Industrial Electrification and Low Carbon Fuels, Feedstocks, and Energy Sources. Emerging technologies could provide notable opportunities to help the industrial sector make cost-competitive step-change reductions in GHG emissions, particularly in applications associated with process heat, the DOE said.

Low-carbon fuels and energy sources include the use of renewable energy sources, nuclear energy (from fission and/or future fusion reactors), concentrated solar power, and geothermal. Low-carbon feedstocks include bio-based and end-of-life materials, the agency said.

Using hydrogen may also be an option. While most hydrogen is currently made from reforming of natural gas, hydrogen production from renewables, nuclear power, or fossil resources with carbon capture can reduce GHG emissions from these existing demand sectors. Hydrogen production using electrolyzers can additionally supply grid services to increase grid resiliency, and hydrogen technologies can also be used for long-duration energy storage.

The electrification of process heat may also be especially important, it noted. In the U.S., process heating consumes more energy than any other manufacturing end-use. “In 2018, a total of 7,576 trillion Btu (TBtu) of fuel, steam, and electric energy were consumed by U.S. manufacturers for this purpose, comprising 51% of total onsite manufacturing energy. In the same year, process heating accounted for 360 million metric tons of CO2e GHG emissions, representing 31% of the manufacturing sector’s total energy-related emissions,” the roadmap says.

Temperature ranges in individual sectors will prove important to this effort, given that about 30% of process heat demand is at temperatures at or below 150C. “Electric technologies like heat pumps, microwave technologies, infrared technologies and other low- and no-carbon sources of process heat such as solar thermal and nuclear could be considered for use in this range,” the DOE said. However, nuclear can go up to 300C, and advanced gas-cooled very-high-temperature reactors can reach 900C at scales that suit distributed applications, it said. Getting these technologies deployed, however, will require RD&D.

Carbon Capture, Utilization, and Storage. The DOE views CCUS as a mitigation strategy for industrial decarbonization. However, CCUS faces constraints. While CCUS has been demonstrated across various sectors, broad-scale deployment of CCUS faces regulatory and economic challenges. The industrial sector faces “high costs for industrial plants in terms of both capital and operating costs,” it said.

CCUS could benefit from more research on better catalysts and process designs to bring higher efficiency levels, lower costs, and lower material consumption or waste production, the roadmap notes. A future national-level CCUS network may also be integral, though more work is needed on pairing and optimizing carbon capture technologies with industrial processes based on CO2 purity and operational considerations of the industrial process.

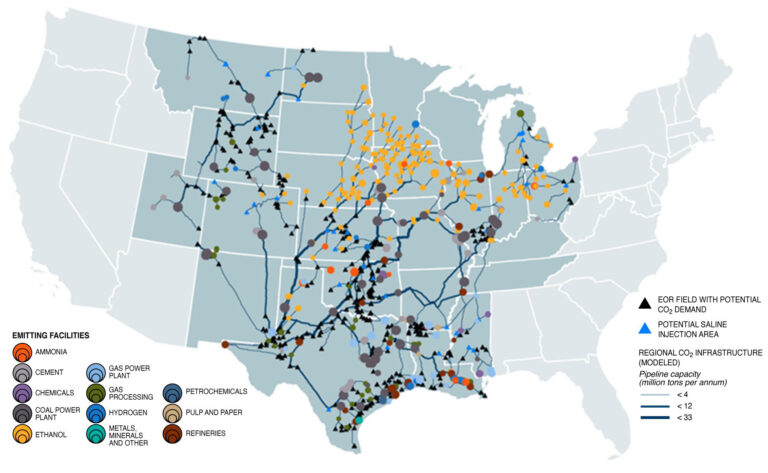

Example of an optimized transport network for economy-wide carbon capture and storage. Source: Great Plains Institute

How Could Industrial Decarbonization Affect the Power Sector?

The DOE’s roadmap is a significant step in a series of recent efforts to encourage industrial decarbonization. In June 2022, DOE established a new $70 million funding opportunity as part of its 2016–established Clean Energy Manufacturing Innovation Institute to develop and scale electrified processes that reduce emissions, improve flexibility, and enhance energy efficiency of industrial process heating. And in April, the DOE launched the Industrial Technology Innovation Advisory Committee, a federal advisory committee charged with advising DOE on industrial emissions reductions technologies.

On Wednesday, key DOE officials noted the initiative goes hand-in-hand with the administration’s larger decarbonization goals, including to achieve 100% clean electricity or a net-zero power grid in the U.S. by 2035.

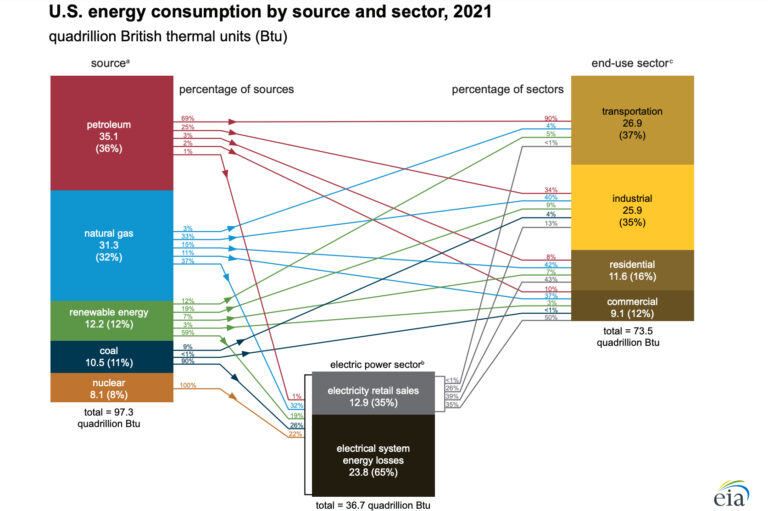

One reason the Biden administration is focused on the industrial sector is that it is considered a “difficult-to-decarbonize” segment of the energy economy, owing to a diversity of energy inputs that feed into its array of industrial processes and operations. The U.S. industrial sector in 2021 consumed nearly a third of the nation’s primary energy and produced 30% of its energy-related carbon emissions, according to the Energy Information Administration (EIA).

The EIA estimates that only 9% of energy consumed by industry came from renewables, while 13% came from electricity retail sales. Industrial consumption, meanwhile, accounted for nearly a quarter of all electricity retail sales.

U.S. energy consumption by source and sector, 2021. Source: EIA

The DOE’s roadmap says the bulk of industrial emissions are attributable to combusted fuel and electricity generation, but also to industrial process emissions, and product lifecycle emissions. The chemicals, refining, iron and steel, mining, and agriculture sectors are by far the largest emitters of industrial emissions.

Decarbonizing the manufacturing sector won’t be easy, it acknowledges. “To decarbonize the industrial sector, the United States will face a range of structural and technical challenges. Considering the sheer magnitude of materials transformations undertaken in industry, from extraction of raw materials to the creation of intermediate and final products, decarbonization will require a wide range of technology solutions that will have a ripple effect across increasingly complex supply chains,” it noted.

How it will affect the power sector, which is in the midst of its own transformation, remains debated. Most industry observers note, however, that if industrial decarbonization leans heavily on electrification, electricity demand could jump substantially. An Aug 30–released report from the National Renewable Energy Laboratory (NREL) that examines supply-side options to achieve 100% clean electricity by 2035 suggests aggressive electrification of end uses—for all sectors, including transportation, residential, commercial, and industrial—could nearly double demand by 2035. Without a boost in energy efficiency, the study projects annual direct electricity consumption in 2035 could soar to 6,200 TWh, compared with 3,700 TWh in 2020.

The report, however, warns that dramatically accelerating the electrification of demand sectors to get the county on the path to net-zero by 2050 could make it “more difficult to decarbonize the electricity system due to the rate of deployment needed.” Still, electrification of buildings, much of transportation, and industry presents “the most cost-effective pathway” to achieving large-scale decarbonization across the economy. “Aggressive energy efficiency and demand management measures can help reduce deployment needs,” NREL noted.