While most of Europe and the wider world have focused on how Russia’s war in Ukraine has impacted oil, gas and, more recently, nickel prices, relatively little has been written about the coal price shock that is likely to hit the region and spread like a tsunami around the world.

Russia is Europe’s largest supplier of thermal coal. According to Eurostat, last year, Russia supplied EU member states with 36 million t of thermal coal, representing 70% of total thermal coal imports. While volumes have stayed about the same, a decade ago, Russian coal imports were just half that at 35%. While total power coal demand has been on a declining trend for the last 10 years, coal-fired power generators in Europe have become increasingly dependent on Russian coal and Russia’s market share has grown substantially over time.

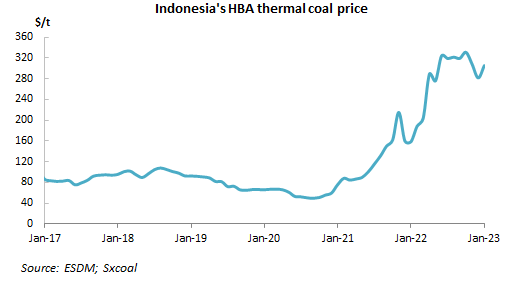

“There is simply an almost complete absence of surplus thermal coal available globally. Prices have shot past US$400 and the US$500/t mark seems to be in play,” says Steve Hulton, VP of Coal at Rystad Energy.

As gas prices continue to soar, European administrations may look to coal to pick up any shortfall in electricity generation as gas usage is scaled back. However, coal consumers will struggle to source additional coal from alternative producers because the supply/demand balance of the international seaborne thermal coal is extremely tight.

How high could prices go?

If sanctions on coal trade with Russia eventuate or there is a physical disruption to Russian rail/port transportation, then the sky’s the limit. Producers and traders are reporting that buyers are already starting to pivot away from Russian coal both in the Atlantic and Pacific markets. And the threat of additional demand and lack of available supply is moving the market. In the last week, coal prices in both Europe and the Pacific have experienced massive jumps. In a sign of just how tight and nervous the market is, a physical trade of Newcastle FOB (6000 kcal) coal was reported last week Wednesday at US$400/t.

Alternative sources: little relief from Colombia, Germany, Poland, South Africa, or the US

Imported coal is generally of better quality and cheaper than any domestic production as all the best coal in Europe was mined out years ago. Germany for example, once a coal mining powerhouse, no longer produces any bituminous coal or anthracite. The last couple of ‘hard’ or ‘black’ coal mines, were closed in 2018 following years of financial subsidies, which were necessary because of high production costs associated with the deep seams and difficult underground mining conditions. Large scale surface mining of low rank (low energy) lignite coal is still carried out, but imported coal is vital to meet the needs of the many thermal power plants designed to burn higher calorific value fuel.

Poland is Europe’s largest remaining coal producer and some 70% of total power generation is sourced from coal. Polish coal production rose slightly in 2021 with the country producing 52 million t of lignite (brown coal), up 13% year-on-year, and 55 million t of hard coal, up 1%. However, the long-term production trend is in decline, and while Poland exports some thermal and coking coal to neighbouring EU countries, it has also increased imports of high energy thermal coal from Russia as it is generally cheaper than local production from deep underground mines.

One of the first places buyers will be calling will be suppliers from Colombia and South Africa. Colombian coal production, which is nearly all exported, recovered in 2021 following a large fall in 2020 due to COVID-19 and a three-month long industrial dispute at the large Cerrejon operation. Production rose to 59.6 million t in 2021, up from 49.3 million t the prior year but still well short of the almost 80 million t it achieved previously. It is expected that production will increase again this year, potentially making an additional 10 million t available for the export market, particularly as Glencore, now the full owner of Cerrejon, looks to take advantage of market conditions and rack-up value from the acquisition.

South African coal exports have been below planned levels for a number of years. Exports fell below 60 million t last year, the lowest level in decades as the rail network was severely hampered by theft of copper cable. Annual exports of 70 to 75 million t should be achievable if railway operator Transnet can sort out its security issues.

US coal production is currently seeing a resurgence after several years of decline, boosted by strong coal demand and robust prices, both domestically and overseas. Based on EIA figures reported to 3Q21, US thermal coal producers were on track to end up exporting approximately 36 million t last year, a hefty 30% increase from 2020. Only around 5 million t were destined for Europe as Asian markets again proved a popular and growing destination. With a lack of investment in new mining areas and a general avoidance of the sector by investors, several US mines have closed in recent years, which will hamper the ability to ramp up additional coal for a rampant European market, particularly when US power stations are paying high prices for domestic supply.